The recent collapses of Signature Bank and Silicon Valley Bank will mean increased focus from both regulators and auditors as financial institutions finalize 2022 results and prepare 2023 first-quarter results. Focus areas will include:

- Significant deposit balances in excess of FDIC insurance limits, including brokered deposits

- Significant concentrations of deposit balances, including groups of related customers such as certain industries

- Trends in deposit balances, e.g., monthly trend of increasing withdrawals

- Significant unrealized losses on held-to-maturity (HTM) securities, especially those that would change regulatory capital classifications from well capitalized to undercapitalized

Bank regulators have reacted quickly to calm markets and created a new liquidity facility for financial institutions.

What Happened?

To curb the inflation triggered by the COVID-19 pandemic and supply chain issues, the Federal Reserve began to quickly raise interest rates in 2022. A rising interest rate environment increases risks on banks’ investment portfolio valuations, noninterest income sources, and deposit stability. A financial institution’s asset/liability risk management is critical to successfully navigate current economic conditions. The extent of a mismatch between the maturity or repricing of assets and liabilities will determine an institution’s exposure to interest rate risk. While banking regulators recently issued a joint statement warning about liquidity risks, the recent quickness and scale of deposit runs caught many by surprise.

Source: fdic.gov

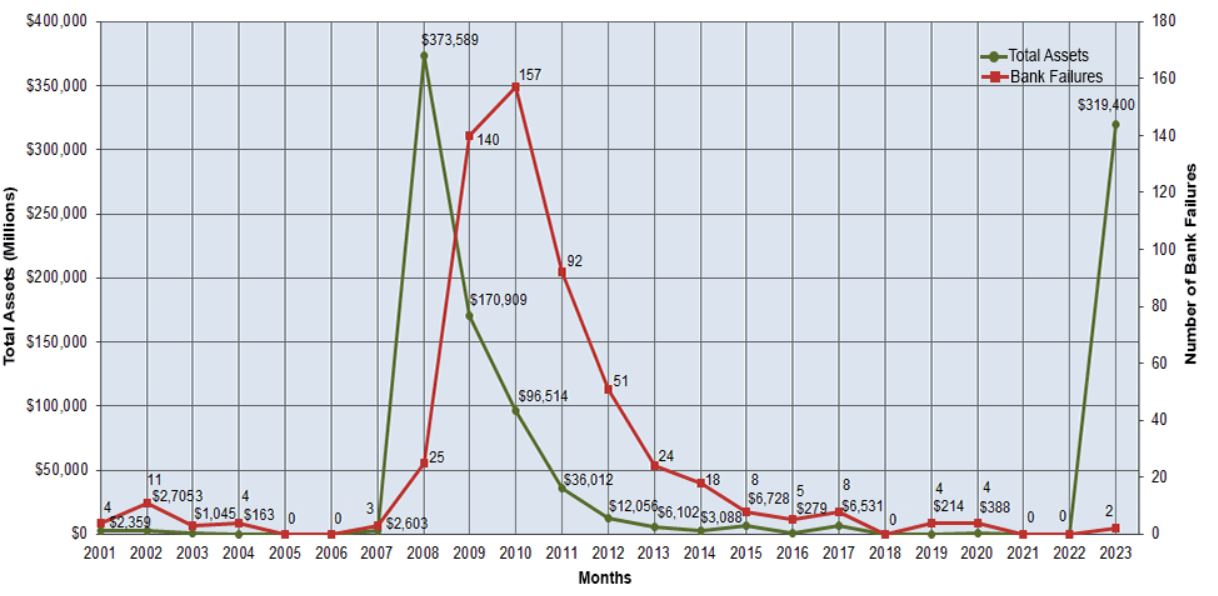

Silicon Valley Bank with $209 billion in assets is the second largest bank failure after Washington Mutual’s $306 billion collapse in 2008.1 Washington Mutual was placed into receivership after depositors withdrew $17 billion and the bank had limited ability to borrow cash from the Federal Home Loan Banks to meet demand. Silvergate Bank, which focused primarily on crypto industry customers, saw a drop of 70% of its deposits in the fourth quarter 2022 due to fallout from the November FTX collapse and was forced to sell investment holdings at a loss of $718 million to meet that demand. Silvergate began liquidation proceeding before any FDIC intervention. For Silicon Valley Bank, a run started when the bank announced it was raising capital. Within days, $42 billion of deposits were withdrawn, leading the FDIC to step in on March 10. Signature Bank, with $110 billion in assets, also was tainted by the November FTX collapse. Regulatory filings indicate that more than $79 billion of Signature Bank’s roughly $88 billion in deposits were uninsured at the end of last year. On March 12, 2023, the FDIC intervened under a systemic risk exception.

The federal government has reacted quickly to calm markets. The FDIC will make depositors of both banks whole, but unlike the 2008 mortgage crisis, investors and bondholders will bear the losses without any taxpayer bailouts. The new Bank Term Funding Program will offer loans of up to one year to any U.S. federally insured depository institution (including banks, savings associations, and credit unions). U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets can be posted as collateral and valued at par. Margin will be 100% of par value. This facility will be available until March 11, 2024 and should eliminate an institution’s need to sell securities at a loss.

FORVIS will continue to follow this developing situation. For questions or to learn more, reach out to a professional at FORVIS or submit the Contact Us form below.

- 1“One of Silicon Valley’s top banks fails; assets are seized,” apnews.com, March 12, 2023