More than 30,000 entities—primarily state, local, and tribal governments—have received funding as part of the U.S. Department of the Treasury's (Treasury) $350 billion Coronavirus State and Local Fiscal Recovery Funds (CSLFRF) program. Generally, recipients that spend $750,000 or more in federally granted aid each year are subject to a Single Audit. However, many CSLFRF funding recipients are very small local governments that may previously have had little to no experience with Single Audits. To lighten the burden on these smaller organizations, recipients that expend $750,000 or more of federal awards during the recipient’s fiscal year and that meet both criteria below have the option to follow the alternative CSLFRF compliance examination engagement as of April 8, 2022:

- The recipient's total CSLFRF award received directly from Treasury or received (through states) as a non-entitlement unit of local government is at or below $10 million; and

- The recipient expended less than $750,000 in other federal awards (not including CSLFRF funds) in the recipient's fiscal year.

The alternative engagement, which is required to be performed under the AICPA's attestation standards and Government Auditing Standards, will focus on two narrowly scoped compliance requirements related to Activities Allowed and Unallowed and Allowable Cost/Cost Principles.

For organizations that are subject to a Single Audit this year, below is a summary of the updates in the 2022 Compliance Supplement.

Key 2022 Compliance Supplement Changes

Programs Added in 2022 that were excluded in 2021:

- 14.888 – Lead-Based Paint Capital Fund Program and Housing-Related Hazards Capital Fund

- 21.023 – Emergency Rental Assistance (ERA)

- 21.026 – Homeowner Assistance Fund

- 21.029 – Coronavirus Capital Projects Fund

- 32.009 – Emergency Connectivity Fund

- 59.075 – Shuttered Venue Operators Grant (SVOG)

- 93.671 – Family Violence Prevention and Services/Domestic Violence Shelter and Supportive Services

Changes to existing programs are as follows:

- 84.425 – Education Stabilization Fund (ESF) – Section 2 – Added Cash Management as applicable for Higher Education Emergency Relief Fund (HEERF) funding, which was primarily provided to institutions of higher education.

- 21.027 – CSLFRF – Revisions were added to incorporate the CSLFRF Final Rule. Clarified that the expenditures reported on the SEFA should not be the total amount of the lost revenue calculated for this program, but the amount of expenditures for government service. Added guidance for the alternative compliance examination engagement that can be completed if 1) the recipient’s CSLFRF award is below $10 million and 2) all other federal awards expended in the fiscal year are less than $750,000.

- 93.498 – Provider Relief Funds (PRF) – Guidance was added regarding the removal of the Special Tests and Provisions requirement and clarifies lost revenue reporting on the SEFA.

- 59.075 – SVOG – Activities Allowed, Allowable Costs, and Period of Performance are the only applicable compliance requirements. Notice was provided that audits of for-profit entities with SVOG would be forthcoming from the U.S. Small Business Administration (SBA) and auditors should only use the Compliance Supplement for nonprofit or governmental entities.

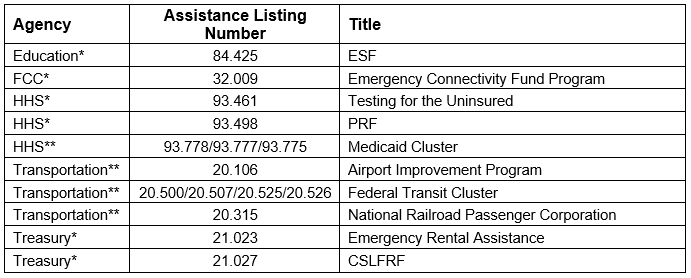

Higher Risk Programs

Below is a complete list of programs with COVID-19 funding that have been identified as “higher risk” for audits subject to the 2022 Compliance Supplement. A “higher risk” designation often (though not always) results in a program or other cluster being audited.

*Programs created by one of the COVID-19 acts and thus considered 100% COVID-19 funding.

**Existing programs that received additional funding from one or more of the COVID-19 acts.

How can FORVIS Help?

According to data compiled by the OMB via the Federal Audit Clearinghouse, FORVIS is a leading provider of Single Audits among CPA firms. Whether you’re preparing for your first Single Audit or you’ve had Single Audits for years, our professionals can help you navigate the Uniform Guidance regulations and compliance requirements, develop internal controls, and gather the necessary information that will help your Single Audit go more smoothly.

As with most topics related to COVID-19, changes are being made rapidly. Please note that this information is current as of the date of publication. Reach out to a professional at FORVIS or submit the Contact Us form below if you have questions.