The Inflation Reduction Act (IRA) and CHIPS Act of 2022 (CHIPS) provide eligible taxpayers options to monetize clean energy and semiconductor manufacturing tax credits: direct pay and credit transfer. The IRS is requiring taxpayers to register their intention to make a direct pay or transfer election via its recently released Pre-Filing Registration Tool. After registering on this portal, taxpayers should include the resulting registration numbers on their timely filed annual tax returns to properly make the direct pay or transfer credits election and successfully transfer credits or receive an elective payment. The opening of the Pre-Filing Registration Tool portal allows taxpayers to now begin to monetize their credits earned in tax years beginning after December 31, 2022.

Background: What Are the Options?

Direct Pay Election

For tax-exempt entities that largely do not have taxable income to offset with credits, a direct pay election is available. This election allows these entities to receive cash back equal to what otherwise would be allowed as a tax credit for their investments in clean energy projects. This monetization option has brought, for example, nonprofit universities and healthcare systems into the fold of clean energy incentives.

Taxable entities may also receive an elective payment for these specified clean energy credits: Sections 45X, 45Q, and 45V. Taxable entities that claim one of these credits should consider various factors when determining whether it is more favorable to claim the income tax credit now or in the future, sell the credit (presumably at a discount), or receive an elective payment (allowing for the related waiting period for filing and receiving cash from the IRS). Taxable entities also may receive an elective payment for manufacturing credits earned under CHIPS.

Credit Transfer

Taxable entities can now sell certain clean energy credits to third parties. If the entity is in a loss position or anticipates being unable to utilize the tax credits in the future, they may now receive the benefit of cash from the sale of credits. Although the sale will presumably be discounted, this monetization option still allows sellers to benefit from their clean energy investments regardless of their federal income tax liability.

Who Can Make Elections? Who Should Use the Portal?

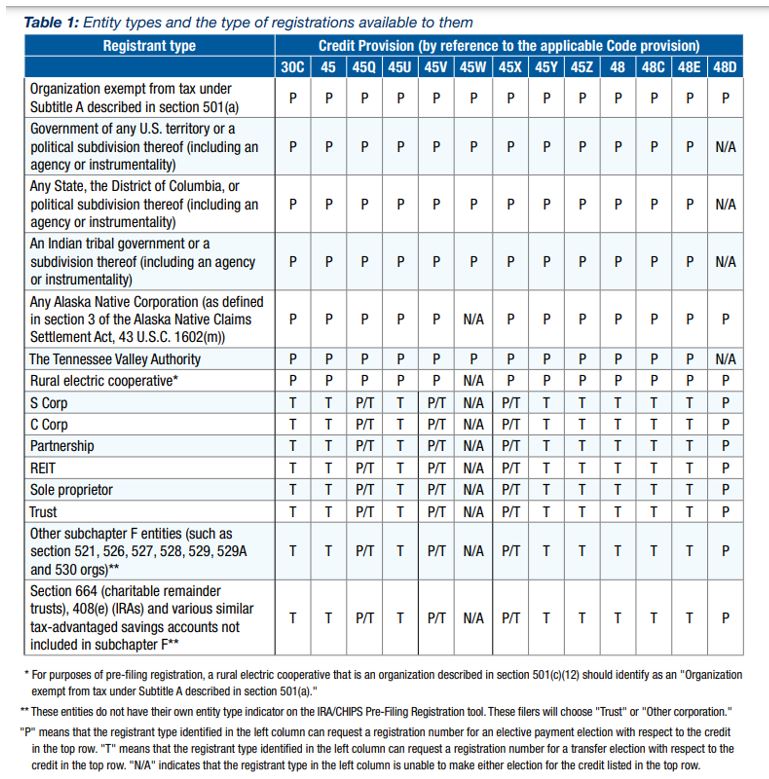

The IRS table below summarizes which credits are available for direct pay or transfer by entity type:

Source: https://www.irs.gov/pub/irs-pdf/p5884.pdf

What Is the Portal For?

To elect direct pay or credit transfer, taxpayers must complete the pre-filing registration process through the IRS’ pre-filing tool. The IRS has issued Publication 5884, which provides details on the process and a taxpayer user guide. It is important to note that registration cannot be submitted until the property or facility is placed in service. This publication also includes important considerations for taxpayers:

- “The IRS intends to review and process registration submissions through the IRA/CHIPS Pre-Filing Registration tool in the order it receives them. A registrant cannot request expedited handling.

- If the registrant chooses to make additional pre-filing registration submissions for different facilities/properties, the registrant must wait until the most recent pre-filing registration submission is processed by the IRS and returned.

- IRS may consider a registrant’s tax period ending date when managing the pre-filing registration caseload.

- The IRS will work to issue a registration number even where the registration submission is made close in time before the registrant’s filing deadline. In such cases, the registrant should anticipate that the tax return on which the elective payment or transfer election is made may undergo heightened scrutiny to mitigate the risk of fraud and duplication that pre-filing registration is intended to address before a payment is issued.”

Note that a separate registration number should be pursued for each clean energy property or project as appropriate for different credits. Given the second bullet point above, taxpayers should expect and plan for the lag in time to register their various projects that year. In addition, it should be noted that while amendments to a registration may be necessary, a registration submitted for review cannot be changed until it is returned with registration numbers or comments that explain why registration numbers were not issued. Finally, the IRS recommends taxpayers monitor the status of their submitted registrations on a weekly basis while under review.

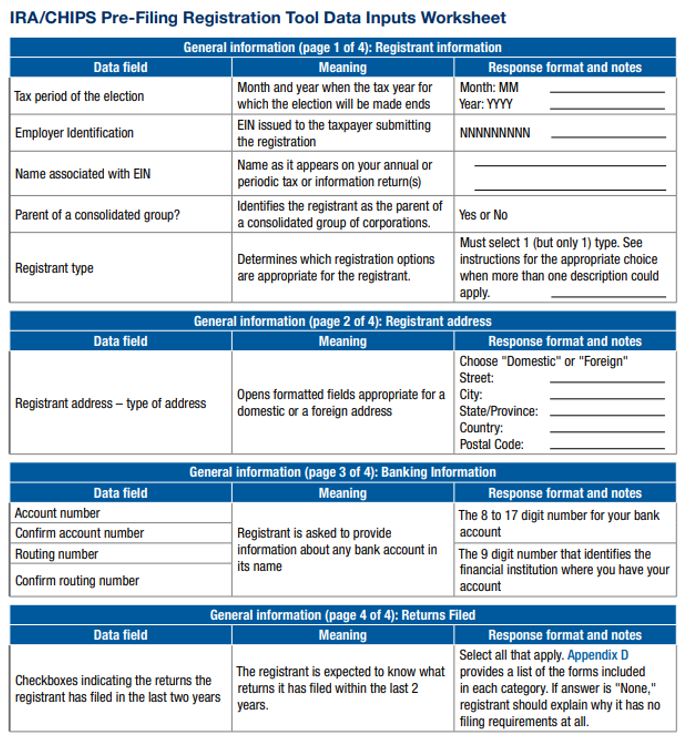

What Information Do I Need for Pre-Registration?

Each registrant will need to provide both general entity information and credit-specific information. The credit-specific information varies depending on which credit is pursued. While credit-specific requirements are available in Publication 5884, common information required among various credits includes:

- Choice of Election

- Subsidiary in a Consolidated Group of Corporations

- Important Dates

- Date Construction Began

- Date Placed in Service

- Facility/Property Location

- Joint Ownership

- Source of Funds

- Additional Information

As stated above, a separate registration is required for each facility/property. However, the IRS will allow bulk uploads of facility/property information by way of a spreadsheet file for certain credits, i.e., Sections 30C, 45, 45W, and 48.

The chart below summarizes the general entity information taxpayers must include in the portal for registration:

Source: https://www.irs.gov/pub/irs-pdf/p5884.pdf

Proposed regulations that speak to general requirements for an effective credit transfer or direct pay election also are available. Consult with your FORVIS advisor on these considerations, including topics such as timing and form of payment for credit transfer, and documentation requirements for each option.