A dealmaker approaching the closing table without having contemplated the difference between month-end and mid-month working capital balances could be facing significant purchase price adjustments, insufficient working capital, or a delay in closing.

In preparation for a transaction, the financial due diligence team will often aid its client in preparing an estimated target of working capital to be delivered with the business at close. This is often referred to as the “working capital mechanism” or the “working capital peg.” Understanding the normalized working capital needed to operate the business helps to provide that the seller delivers sufficient working capital to transition the business to the buyer with little interruption. The working capital mechanism is often estimated as the average of the adjusted trailing 3-, 6-, or 12-month ending balances and uses a month-end basis as it mirrors the financial reporting cycle, aligns with the presentation of other monthly due diligence procedures, and is generally derived from readily available data.

However, dealmakers should be aware of working capital differences throughout a month and anticipate that a working capital peg based on month-end balances may not approximate what a seller should be expected to deliver at a mid-month closing date. While the timing of routine transactions can create working capital differences, other accounting policies can result in the need to contemplate components that may not have been previously reported on the balance sheet.

Items Not Reported at Month-End

Many of today’s technology, services, and telecommunications companies have adopted the practice of billing monthly customers at the beginning of the month, in advance of providing that month’s services. Often, the customer obligation associated with those services would be fully satisfied within the month resulting in no deferred revenue at month-end. The seller has collected cash, fully performed on its obligation and, all else equal, the buyer will likewise invoice and collect in the days after close, generating a sufficient amount of working capital to fund that month’s operations.

However, should the deal close at a mid-month date, the sufficiency and treatment of deferred revenue, which was never a component of a month-end balance sheet, needs to be reevaluated as the balance of deferred revenue may be higher during the month than it would be at month-end. The obligation to the customer would have only been partially satisfied despite having been paid in full. A buyer would now find itself with a portion of that month’s service yet to be delivered and may incur costs to provide services without receivables or cash to offset those costs. Intra-month settlements should be considered so the seller maintains sufficient cash in the business to service unsatisfied customer obligations. Deferred revenue can be excluded from the peg and treated as a debt-like item to be settled at close in a transaction contemplated on a cash-free, debt-free basis.

In other situations, companies may invoice customers for services in arrears, which may impact working capital mechanism considerations. A software-as-a-service (SaaS) business that bills its customers in arrears on the first of the month for the prior month’s services should recognize revenue throughout the month as services are provided and report unbilled receivables—a component of net working capital—until the time of billing. However, for a company with limited users of financial statements, this level of reporting may not be necessary as the perceived value for the management team may be limited. In this instance, the company likely reports receivables when billed, resulting in understated balance sheets and out-of-period revenue. If a seller starts to feel that an inequity exists as a result of having borne the costs to provide a partial month of services but been unable to bill, a deal issue could arise. If unbilled receivable balances are not included in the estimated working capital peg, including them in delivered working capital at a mid-month close date would be improper and could result in the seller ultimately walking away with more than 12 months of revenue-related cash for providing 12 months of services.

In addition, routine monthly transactions may result in significant differences in working capital at month-end compared to mid-month balances. The balance of prepaid rent, if paid at the beginning of a month, could be a routine adjustment to derive working capital delivered in the middle of a month that may not have been considered in the working capital peg if set based on month-end balances. Similarly, certain expenses should be accrued ratably during the month, which would result in lower accrued expenses and thus higher working capital during the month in comparison to month-end.

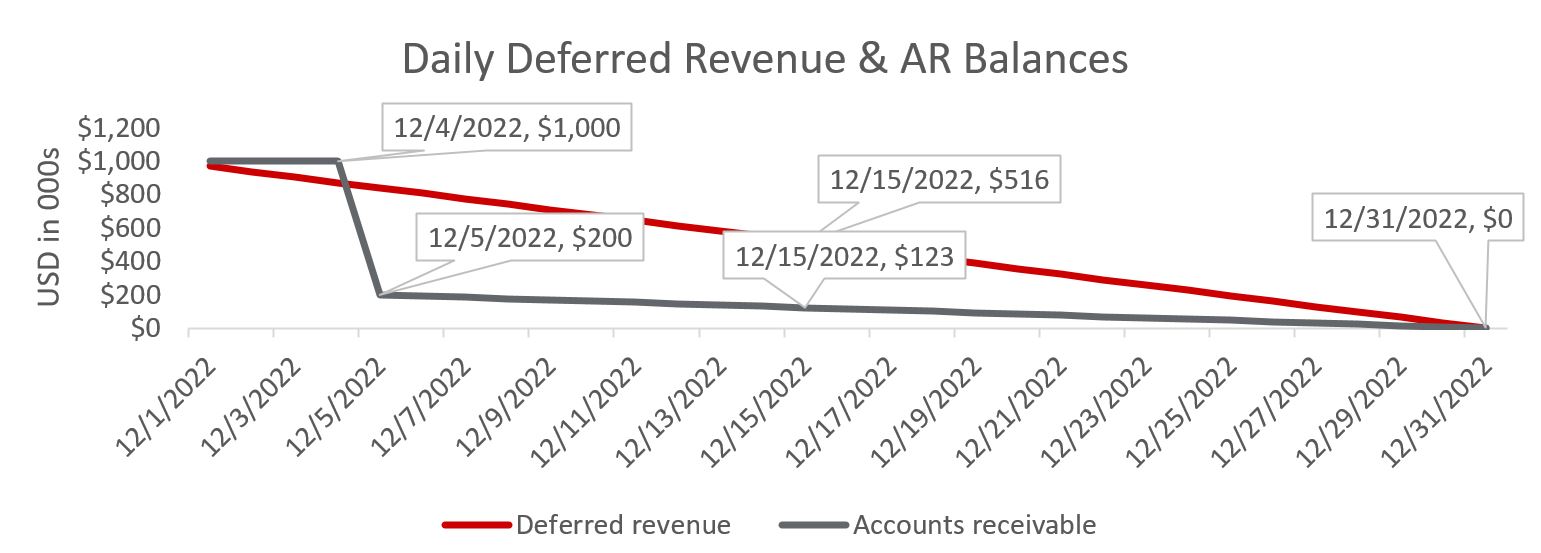

The table above presents the fluctuating daily deferred revenue and accounts receivable balances for a services company that (i) provides services ratably across the month, (ii) bills its customers in advance on the first of the month, (iii) collects 80% of receivables via credit card charges on the fifth of the month, and (iv) collects the remainder of receivables ratably throughout the month and represents how working capital can fluctuate on a daily basis.

Final Thoughts

It can be easy to get the working capital estimate wrong when the closing date does not tightly align with the basis on which the peg was contemplated. While these types of issues can appear as surprises when a mid-month close is not expected, being aware of how working capital fluctuates throughout the month can prepare a dealmaker to closely estimate the amount of working capital to be delivered at a mid-month close. A skilled advisor needs to anticipate that a mid-month close is likely and prepare early in the process by asking the right questions, understanding the key transaction drivers, and ultimately helping their client feel confident they are leaving nothing on the table. If you are contemplating a transaction or feeling as if a prior transaction lacked the forward vision needed to navigate these issues, FORVIS has a fully dedicated team of deal professionals who aim to provide an Unmatched Client Experience™.

Reach out to your professional at FORVIS or submit the Contact Us form below for assistance.