Earlier this year, the U.S. federal government closed the commentary period for a proposed regulation, Federal Acquisition Regulation (FAR) Case 2021-015,1 that could fundamentally change federal contracting. Under this proposed rule, many federal contractors would be required to report their organization’s greenhouse gas (GHG) emissions. While some contractors previously reported their GHG emissions voluntarily, the proposed rule would compel many remaining contractors to publicly report their emissions. In addition to GHG disclosures, hundreds of contractors also will need to establish GHG reduction targets. These efforts would require significant preparation and investment for companies that are early in their GHG reporting journey or that have not reported GHG emissions yet. Suppliers and subcontractors to major government contractors also would need to inventory their GHG emissions. Even though the rule is only proposed, some federal government requests for proposal (RFPs) already feature the same or similar considerations in proposal evaluation criteria.

There are steps that government contractors can take in the near term to meet contracting officers’ expectations for GHG emissions performance and reporting while also preparing for the finalization of FAR Case 2021-015. Contractors unfamiliar with how to report GHG data should start by conducting a GHG inventory. In addition, they should study the Task Force on Climate-related Financial Disclosures (TCFD) and the Science Based Targets initiative (SBTi) frameworks and requirements and understand how to disclose emissions data conforming to the CDP (formerly the Carbon Disclosure Project) climate change questionnaire.

Background of Proposed GHG Reporting Rule

In May 2021, the Biden administration signed Executive Order (EO) 14030 requiring GHG disclosure requirements to be incorporated into the FAR. The EO expects “major Federal suppliers to publicly disclose GHG emissions and climate-related financial risk and to set science-based reduction targets.” The EO also directs “that major Federal agency procurements minimize the risk of climate change, including requiring the social cost of GHG emissions to be considered in procurement decisions and, where appropriate and feasible, give preference to bids and proposals from suppliers with a lower social cost of GHG emissions.”2

The Office of Management and Budget encouraged the FAR Council to leverage existing third-party standards such as the CDP, TCFD, and SBTi to develop the GHG disclosure policy.3

Proposed GHG Emissions Reporting Requirements

Significant & Major Contractor Actions Under Proposed Requirements

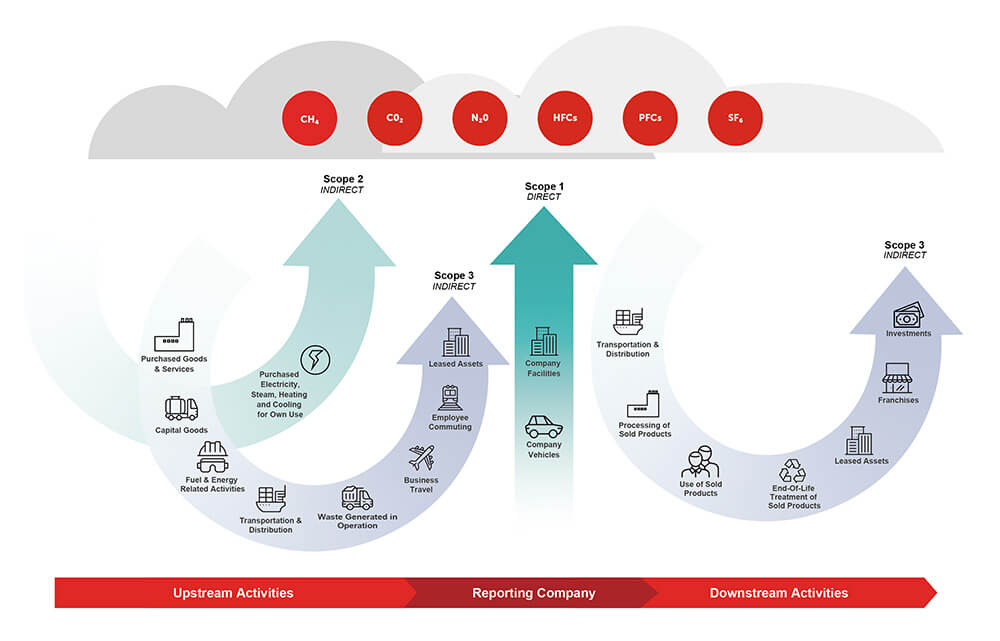

Under the proposed requirements,4 contractors that received awards between $7.5 million and $50 million in the prior federal fiscal year, i.e., significant contractors, and contractors that have received more than $50 million, i.e., major contractors, will be required to complete a GHG inventory by determining material Scope 1 emissions sources and calculating electricity consumption for Scope 2 calculation requirements.5 The following figure provides an overview of GHG Protocol scopes and emissions across the value chain.

Source: Adapted from the ghgprotocol.org6

The FAR Council estimates less than 5% of significant contractors have disclosed GHG emissions previously.7 While many major contractors have voluntarily disclosed GHG emissions, the federal government estimates major contractors that currently lack a GHG inventory would on average need to spend $508,000 in the initial year, then more than $400,000 in subsequent years to align with the proposed rule.8 Regardless of prior GHG report disclosures, contractors would have one year after the final rule has been published before being obligated to report GHG emissions.

Major Contractor Actions Under Proposed Requirements

In addition to providing Scope 1 and 2 emissions, major contractors would have five additional requirements that come into effect two years after the final rule has been published, including:

- Measure and report Scope 3 GHG emissions annually in the System for Award Management (SAM), which is the platform where contractors can find opportunities, track awards and disbursements, and submit post-award reports.

- Complete the CDP climate change questionnaire annually, responding to the questions aligned with the TCFD.9

- Develop a science-based emissions reduction target through the SBTi by submitting a letter to SBTi to be recognized as “committed” on the SBTi website.10

- After the commitment is published on the SBTi website, the company must submit its science-based GHG reduction target for validation by SBTi within 24 months.

- Disclose the following on a publicly accessible website:

- Scope 1, 2, and 3 emissions;

- Annual CDP climate change questionnaire;

- Progress toward submitting a science-based target that has been validated by SBTi.

The SBTi validates organizational low-carbon transition plans and publicly tracks whether those plans are aligned with the Paris Climate Accords. Federal contractors subject to the proposed rule should conduct a gap assessment against SBTi disclosure recommendations.

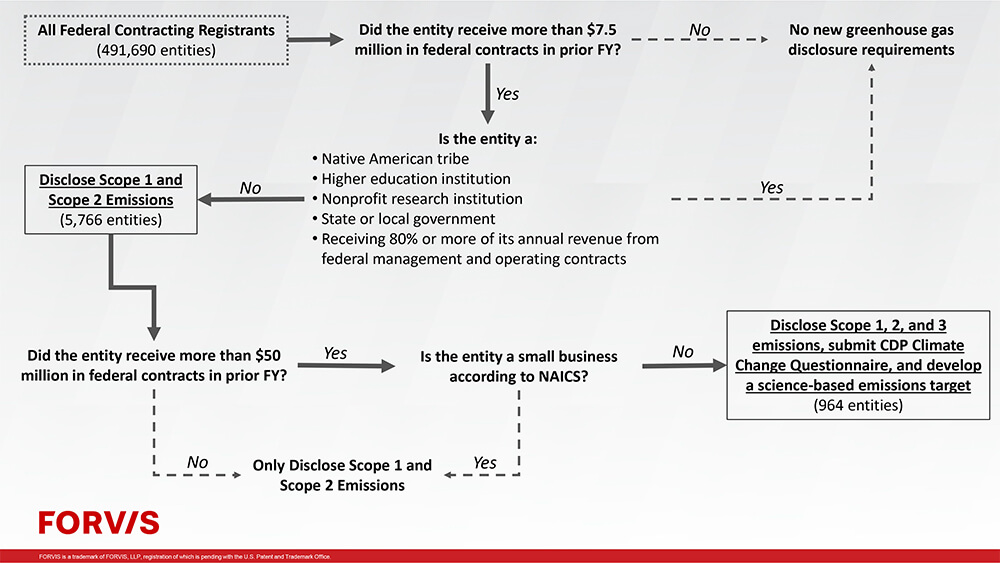

The following figure is a decision tree for determining which GHG disclosures would be required for major and significant federal contractors, including exemptions and the number of affected organizations.

Preparing for the Proposed Emissions Reporting Rule

Even though the regulation is not final, GHG emissions disclosures are already appearing in RFP evaluation criteria. With this in mind, affected federal contractors should be preparing inventories and disclosures of their GHG emissions now.

Suppliers to major government contractors also should be attentive to the proposed regulation, given the supply chain implications of GHG emissions. The ability to quantify emissions and make progress toward reductions are increasingly needed to be competitive in the marketplace. Since major government contractors would be required to assess primary supplier emissions for their Scope 3 requirements, the obligation to report and reduce emissions in accordance with SBTi also would flow down the supply chain to suppliers.

In the near term, government contractors subject to the proposed rule and unfamiliar with how to report GHG data should start by identifying their emissions sources.11 In addition, major contractors subject to the proposed rule should understand the TCFD reporting framework and the SBTi requirements, while also preparing to disclose emissions data consistent with the CDP climate change questionnaire.

By taking the necessary steps to become familiar with reporting GHG data and helping ensure compliance with the proposed requirements, government contractors can fulfill a key directive from EO 14030, provide greater emissions transparency, help their organizations manage climate-related financial risks, and prepare their organizations for setting science-based GHG reduction targets.

If you have any questions or need assistance, please reach out to a professional at FORVIS or use the Contact Us form below.

Related Reading

- Accounting for Climate: The Financial Reporting Requirements You Need to Prepare for Now

- Climate Change Has Broad Economic Implications Now & in the Future – How Will It Affect Your Business?

- 1Federal Acquisition Regulation (FAR): Disclosure of Greenhouse Gas Emissions and Climate-Related Financial Risk.

- 286 FR 27967.

- 3M-22-06: Catalyzing Clean Energy Industries and Jobs Through Federal Sustainability.

- 4FAR Case 2021‐015: Disclosure of Greenhouse Gas Emissions and Climate‐Related Financial Risk Regulatory Impact Analysis, p. 4.

- 5Exceptions: Many Native American tribes, colleges and universities, nonprofit research institutions, and state and local governments, as well as entities receiving 80% or more of their annual revenue from federal management and operating contracts, would be exempt from the new reporting requirements, according to the proposed rule.

- 6WRI/WBCSD Corporate Value Chain (Scope 3) Accounting and Reporting Standard (PDF), p.5.

- 7FAR Case 2021‐015: Disclosure of Greenhouse Gas Emissions and Climate‐Related Financial Risk Regulatory Impact Analysis, p. 45-46.

- 8FAR Case 2021‐015: Disclosure of Greenhouse Gas Emissions and Climate‐Related Financial Risk Regulatory Impact Analysis, p. 40.

- 9FAR Case 2021‐015: Disclosure of Greenhouse Gas Emissions and Climate‐Related Financial Risk Regulatory Impact Analysis, p. 18-19.

- 10 sciencebasedtargets.org.

- 11 “GHG Inventory Development Process and Guidance,” epa.gov.